In Practice News

“IAASA continues to support the highest standards of auditing and corporate reporting quality. This is achieved through our regulatory approach that sets a benchmark in terms of our expectations on quality, and where necessary a robust enforcement policy where there are significant departures from that benchmark. IAASA also maintains quality throughout the profession by the issue of high-quality auditing standards and through its oversight of the regulatory activities of the prescribed accountancy bodies. Looking to the future, IAASA is preparing for the impact of the Corporate Sustainability Reporting Directive and its corporate reporting and assurance requirements. While IAASA is focussing on its public interest entity population, these will in time impact on thousands of companies in Ireland.”

The Market Intelligence & Insights function will focus on providing more comprehensive, evidence-based analysis and insights across the FRC’s policy development, monitoring and regulatory activities. Separately, the new Digital Reporting & Taxonomies function has been established, reflecting the importance of these rapidly evolving areas. It will focus on building the FRC’s knowledge and capability, improving the quality of digital reporting, and developing tools to support the reporting ecosystem.

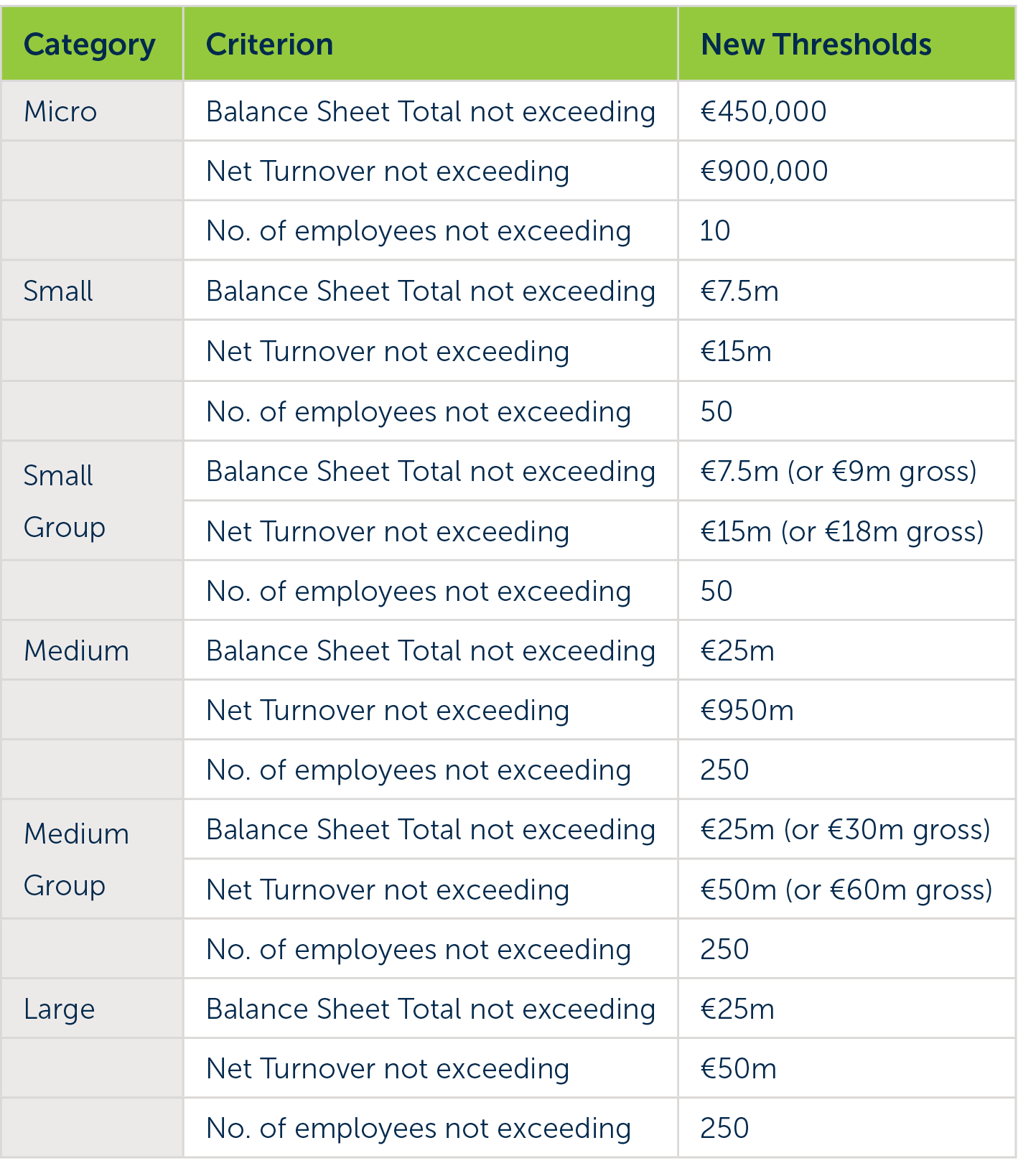

The legislation comes into effect from 1st July 2024 and the measures apply for financial years beginning on or after 1 January 2024, enabling companies to benefit from the adjusted thresholds immediately. Companies may elect to apply the measures on or after 1 January 2023.

Key messages for statutory auditors and audit firms:

- Legislation – Companies Act 2014 – Section 1496 – The legislation explicitly states that a quality assurance review should take place at least every six years.

- Risk Assessment – RABs risk assess statutory auditors and audit firms to determine content and frequency of quality assurance review.

- Timing – A visit may be conducted by the RABs earlier than a six-year interval if deemed necessary or appropriate. Failure to comply may result in regulatory action.

- Final Report on the “Guidelines on Enforcement of Sustainability Information” (GLESI), and

Public Statement on the first application of the European Sustainability Reporting Standards (ESRS). - These documents are designed to support the consistent application and supervision of sustainability reporting requirements across the EU.

The purpose of the GLESI is to provide guidance to build convergence on supervisory practices int the area of sustainability reporting.

Through the Public Statement on the first-time application of the ESRS, ESMA aims to support large issuers addressing the learning curve associated with the implementation of these new reporting requirements.