Value Chain and CSRD Reporting by Sheila Stanley

The CSRD requires value chain reporting, which covers the activities, resources, and relationships the reporting company uses and relies on to create its products or services from conception to delivery, including consumption and end-of- life. Activities, resources, and relationships along the value chain include the following:

- those in the company’s own operations, such as human resources;

- those along its supply, marketing and distribution channels, such as materials and service sourcing and product and service sale and delivery; and

- the financing, geographical, geopolitical and regulatory environments in which the company operates.

Value chain actors are found both upstream and downstream from the company. Actors upstream from the company include suppliers and provide products or services that are used in the development of the company’s products or services. Actors downstream from the company include distributors and customers who receive products or services from the company. In many cases, SMEs will find themselves either as suppliers or distributors in the value chain of a reporting company.

In December 2023, the European Financial Reporting Advisory Group (EFRAG) released a set of guidance documents to help companies comply with the requirements of the ESRS. Of these, the IG 2: Value Chain Implementation Guidance provides useful insights for SMEs in the value chain of large companies to consider.

As actors in the value chain of larger companies reporting under the CSRD, what can SMEs expect to face and how can they prepare themselves?

- Companies that were previously reporting under the Non-Financial Reporting Directive (NFRD) are to report on their FY2024 sustainability performance with limited assurance in the year 2025. Unlike the CSRD, the NFRD did not mandate companies to report on their value chain.

- Other large companies are to report on their FY2025 sustainability performance in the year 2026.

- Listed SMEs are to report on FY2026 performance in the year 2027.

Large companies – both listed and unlisted – refer to an EU undertaking or EU subsidiary of a non-EU entity that satisfies at least two of the following criteria:

- More than €50 million in net turnover (i.e., revenue)

- More than €25 million in balance sheet total (i.e., total assets)

- More than an average of 250 employees during the year

As of 1 January 2024, the ESRS came into effect through the adoption of the Commission Delegated Regulation (EU) 2023/2772 (ESRS Delegated Regulation). The ESRS Delegated Regulation provides details of the sustainability-related disclosure requirements that companies are to report on. The determination of which sustainability matters a company is to report on is based on the principle of double materiality.

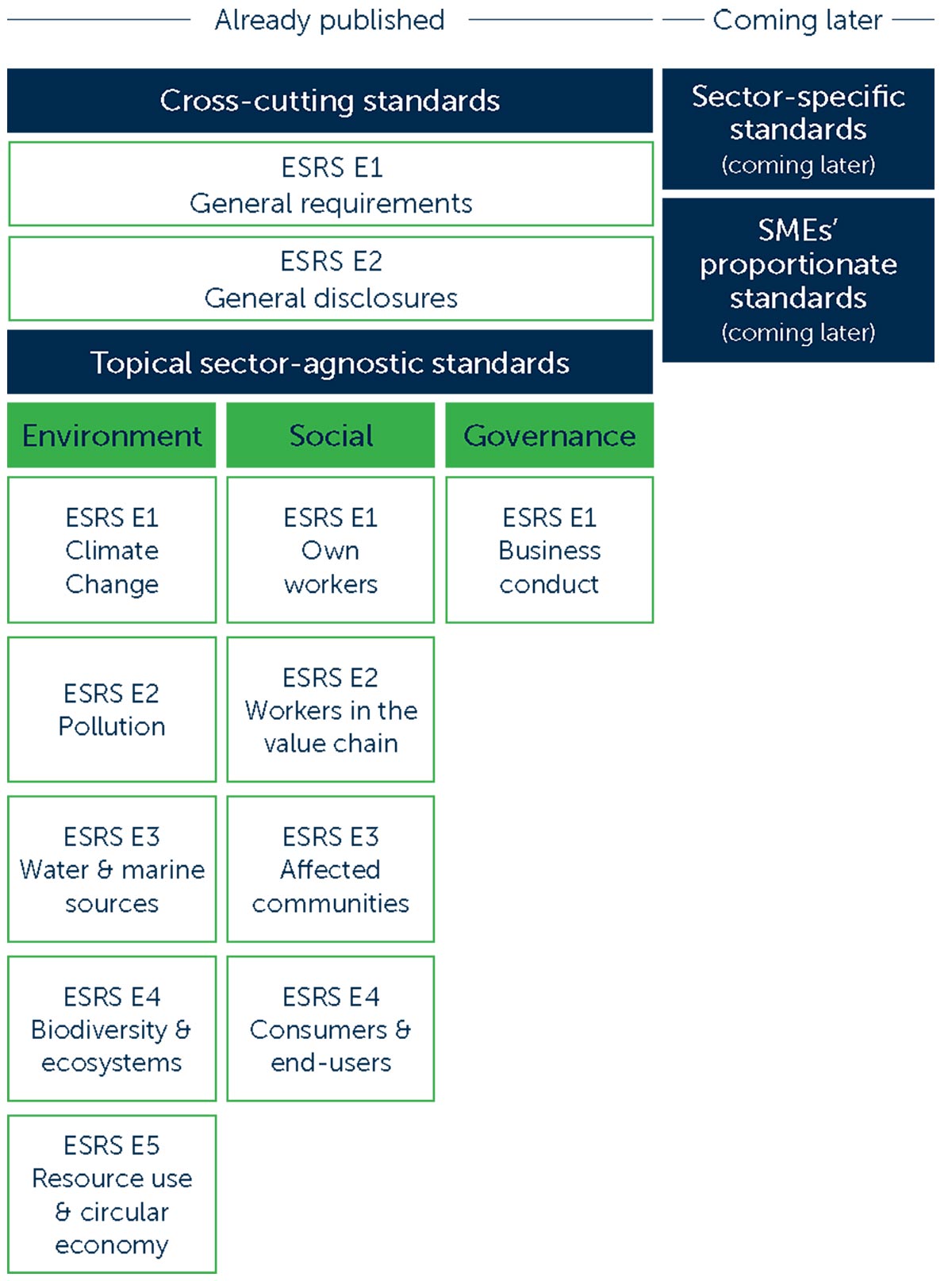

Double materiality essentially refers to two dimensions of materiality – impact materiality which covers the company’s impacts on people and the environment, and financial materiality which covers risks and opportunities related to sustainability matters that affects the company’s development, financial position, financial performance, cash flows, access to finance or cost of capital over the short-, medium- or long-term time horizons The sustainability matters that fall within the scope of the ESRS are wide ranging as outlined in fig 1.

As of the end of 2023 and moving into 2024, many companies that are in-scope for the CSRD for FY2024 have begun their double materiality assessments to ascertain which sustainability matters they will be required to report on. As part of this process, and because the CSRD requires companies to report on the value chain, these companies are reaching out to SMEs such as their suppliers and distributors to obtain their feedback as stakeholders.

The EFRAG IG 2 Value Chain Implementation Guidance provides more clarity in terms of guidance and explanations on value chain disclosures. While the guidance was developed for use by companies that are in-scope under the CSRD and not for SMEs, it does provide some useful points for SMEs to take on board.

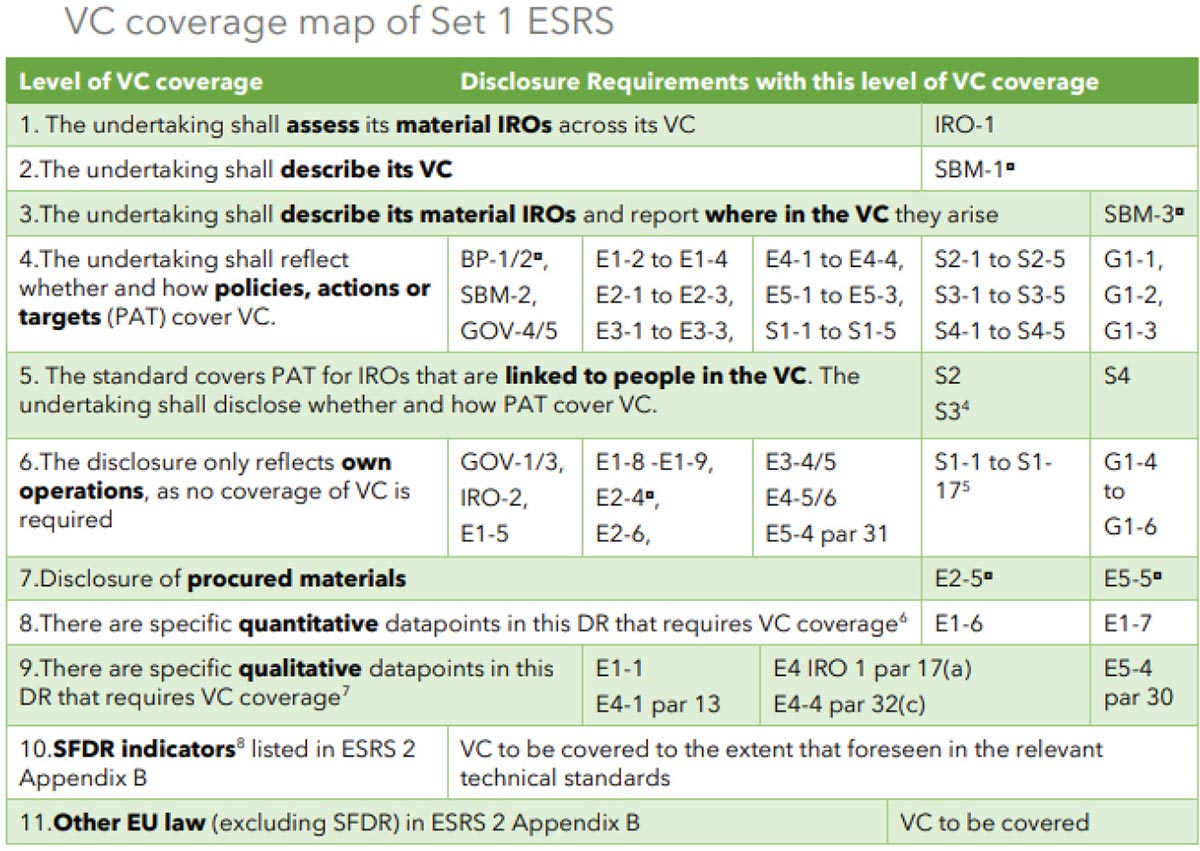

SMEs in the supply chain of companies preparing ESRS reports are considered part of the upstream value chain of the reporting companies, while SMEs that are distributors are considered part of the downstream value chain. The Value Chain (VC) coverage map in the IG 2 provides a snapshot of the specific disclosures within each general and topical standard that requires value chain information (See Figure 2). These cover disclosures under all 10 ESRS topical standards.

IG 2 makes it clear that a company will have to identify risks and opportunities that arise as a result of impacts and dependencies it has on its value chain to provide a fuller picture of its impacts on people and the environment which are connected to its activities, products and services. Effectively, what this means is that a company is to report on the sustainability-related impacts it may have on people and the environment as a result of its business relationships with SMEs such as suppliers and distributors that are involved in its business operations and activities. As an example, SMEs’ greenhouse gas (GHG) emissions that are the result of its business relationships with the reporting company is considered part of the Scope 3 value chain GHG emissions that the large company has to report on.

This means that companies will have no choice but to approach SMEs as part of the double materiality assessment process to obtain their feedback on potential impacts it has on the SME and conversely, to consider the risks and opportunities associated with its SME suppliers.

According to IG 2, companies will have to provide information on how their policies, actions, and targets in relation to each topical standard cover the value chain. By extension, these policies, actions, and targets that companies develop which encompass the value chain will affect how SMEs conduct their own business. SMEs will have to ensure that their own business conduct and activities are aligned with supplier/distributor Environmental, Social and Governance (ESG) and the procurement policies developed by the reporting company.

- Start having the conversation with the reporting company it is a supplier of to find out what the latter’s sustainability considerations are with regards to the products/services provided.

- Find out what information the reporting company will require under the ESRS as a result of its double materiality assessment.

- Review its own processes and systems to gauge its capacity to provide data and information to support the company’s reporting requirements.

- Start thinking about how to incorporate ESG into its business model to ensure its long-term business viability and profitability. An ESG compliant supplier/distributor will become a supplier/distributor of choice for large companies as sustainability reporting requirements further strengthen in the coming years.

- Create awareness and support the dissemination of sustainability knowledge amongst its employees. This will ensure that its employees will be able to effectively engage with the reporting company as well as implement in-house sustainability strategies and development plans that are developed to build out the SME’s sustainability value proposition.

- Adopt the right mindset. Rather than viewing this as a burdensome reporting requirement, SMEs should view this as a strategic investment and opportunity.

- Finally, make the most of government supports available for SMEs to begin their sustainability journey. These include the Green Transition Fund which provides support to SMEs to become more sustainable and prepare themselves for a low-carbon, resource-efficient future through initial planning, capability building, investment, research and innovation.

- Digital and climate transformation projects under the Green Transition Fund are being funded through the EU’s Recovery and Resilience Facility under Ireland’s National Recovery and Resilience Plan (NRPP) 2021-2026.

- Another valuable support available is the Climate Toolkit 4 Business, a toolkit that allows businesses to gauge their environmental impact based on information they have at hand such as energy, water or waste bills and create an improvement plan.

- EFRAG proposes implementation guidance for ESRS (iasplus.com)

- EFRAG IG 2 Value Chain Implementation Guidance. Available at: Download (efrag.org)

- Expected Contributions Of The European Corporate Sustainability Reporting Directive (Csrd) To The Sustainable Development Of The European Union (researchgate.net)

- Delegated regulation – EU – 2023/2772 – EN – EUR-Lex (europa.eu)

- European Sustainability Reporting Standards (ESRS) adopted by EC | EY – Global (Issue 3, August 2023)

- Climate Toolkit 4 Business | Zero Carbon Journey

- Improve sustainability | Business Support | Enterprise Ireland (enterprise-ireland.com)