December 2023

17 Harcourt Street,

Dublin 2, D02 W963

T: 01 425 1000

F: 01 425 1001

Unit 3,

The Old Gasworks,

Kilmorey Street,

Newry, BT34 2DH

T: +44 (0) 28 3025 2771

W: www.cpaireland.ie

E: cpa@cpaireland.ie

Patricia O’Neill

Chief Executive

Eamonn Siggins

Editorial Adviser

Róisín McEntee

Technical Adviser

Phyllis Willoughby

Jenn Brennan

T: 087 203 4202

E: accountancyplus@gmail.com

Caitriona Minogue

T: 086 843 0622

E: accountancyplus@gmail.com

Published by

Nine Rivers Media Ltd.

E: gary@ninerivers.ie

President’s Message

Welcome to the December 2023 edition of Accountancy Plus.

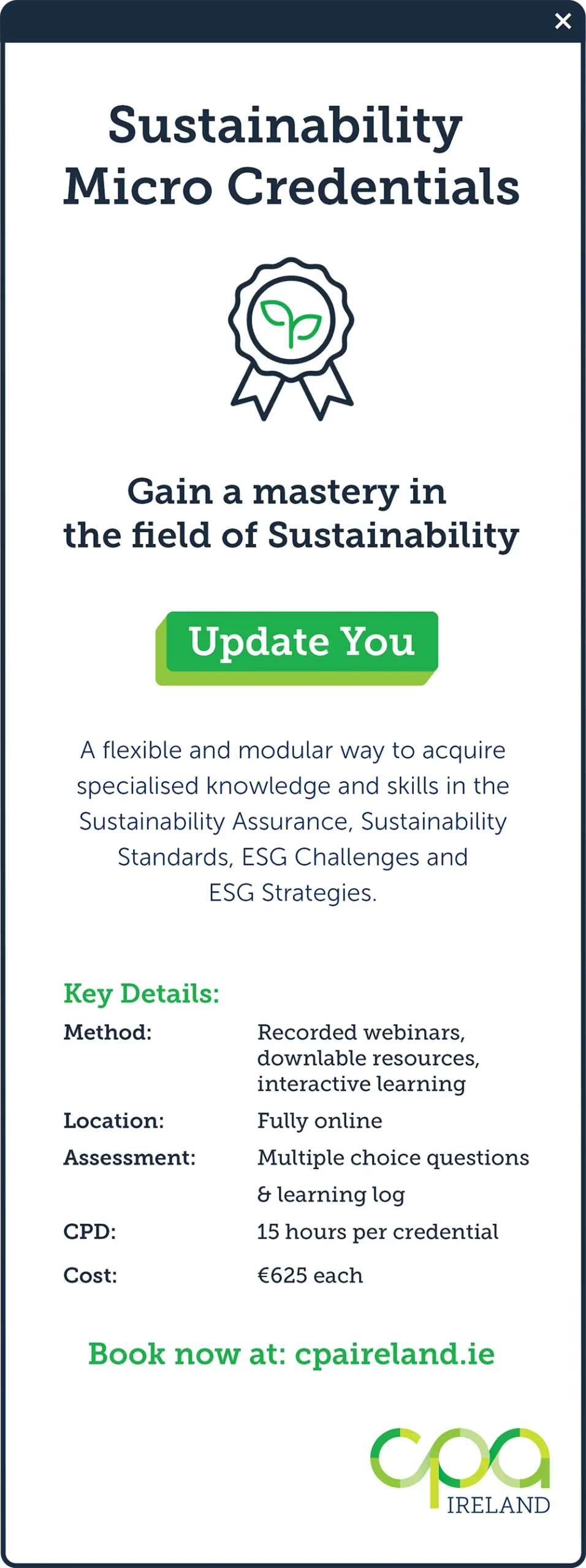

Sustainability Micro-credentials

As the new European Corporate Sustainability Reporting Directive is coming into effect from 2024, it is crucial to stay ahead of the curve and for you to show your commitment to sustainability. Your clients will expect you to help them navigate these new ESG reporting requirements.

To help you in this regard, in September 2023, CPA Ireland launched a series of stackable micro-credentials in Sustainability. These credentials cover Sustainability Reporting Standards, ESG Challenges, ESG Strategies and Sustainability Assurance. You have the option to take individual micro-credentials and complete an online assessment, or you can opt to take all micro-credentials to gain an overall certificate in Sustainability.

CPA Profile

RESEARCH

Are highly integrated performance measures beneficial? by Professor Breda Sweeney

measures beneficial for decision making by senior management teams?

Tools such as the Balanced Scorecard and Performance Prism stress the importance of interlinkages between whatever measures of success are considered critical and advocate the use of an integrated set of key performance indicators (KPIs). Performance measures that are more integrated enable an understanding of how activities link to each other and impact on strategy. In the above example, increasing on-time delivery may be important for ensuring a good firm reputation which in turn will impact on the volume of business and profits. If, however, on-time delivery is not valued by customers and has no impact on firm reputation, then this may not be an area to invest additional resources. For other firms, employee absenteeism may be a critical success factor as reducing absenteeism may impact positively on efficiency, product quality, and employee health and wellbeing, which in turn will improve profitability and ESG performance.

CPA Profile

Ian Quinn

CPA Profile

Ian Quinn

Title: Financial Controller

Company: Kia Ireland

Qualifications: CPA, Diploma in Corporate Governance from UCD Michael Smurfit Business School and a Diploma in Risk Management, Internal Audit and Compliance from Chartered Accountants Ireland

Why did you decide to start out in a career in accountancy?

More importantly, there were 3 people at partner, director and manager level in the practice that positively influenced me in my development as a Trainee Accountant. They also qualified as CPAs at an early age and that encouraged me to complete my CPA exams as quickly as I could. I gained my CPA qualification in 2000 at the age of 23.

Conducting a Scenario Analysis by Sheila Stanley

Climate-related scenario analysis is a tool that enhances critical strategic thinking and allows companies to explore alternatives that may significantly alter the basis for ‘business-as-usual’ assumptions.

Conducting a climate scenario analysis may seem a daunting task for companies that are doing it for the first time. The good news is that IFRS S2 has provisions for proportionate reporting in relation to climate scenario analysis.

Law & Regulation News

Rethinking Regulation to Prioritize Impact

Policymakers currently rely on simple metrics (quantitative criteria) such as turnover, balance sheets, number of employees to categorise and define enterprises. This determines how EU law applies to them. But in today’s world of climate urgency, multiple tensions and disruptive innovations, these metrics fall short.

The breach allowed hackers to access the personal data of millions of people and exposed UK consumers to the risk of financial crime.

In 2017, Equifax’s parent company, Equifax Inc, was subject to one of the largest cybersecurity breaches in history. Cyber-hackers were able to access the personal data of approximately 13.8 million UK consumers because Equifax outsourced data to Equifax Inc’s servers in the US for processing.

The UK consumer data accessed by the hackers ranged from names, dates of birth, phone numbers, Equifax membership login details, partially exposed credit card details, and residential addresses.

Anti-Money Laundering (AML) by Kevin Kerrigan

With respect to specific AML requirements, I often use the 5 Pillars of Compliance as a tool to help accountants understand the policies, controls and procedures they need to put in place to achieve compliance. The 5 pillars and underlying elements should help you answer the “What do we need?” question.

The Consultative Committee of Accountancy Bodies – Ireland (CCAB-I) has developed detailed guidance to help accountants understand their AML obligations within the Irish legal framework. This is another valuable resource when working to further understand your needs and requirements.

Law & Regulation

Navigating Capital Reduction in Business Sales: Avoiding Pitfalls by Brendan Ringrose

Navigating Capital Reduction in Business Sales: Avoiding Pitfalls

by Brendan Ringrose

In the world of takeovers and share sales, advisers face a common challenge. Buyers seek core assets and business from the target company but are keen to dispose of non-core assets beforehand. Pre-sale reorganisation becomes crucial to divest the non-core assets and pave the way for a successful transaction. Brendan Ringrose, Partner in Whitney Moore Law Firm, specialising in Corporate transactions, discusses the legal issues.

In this process, shareholders of the target company should consult taxation advisers to understand any potential liabilities, including capital gains tax and stamp duty. In some cases relief from these taxes may be claimed, subject to specific exceptions and conditions. However, there are legal questions to address such as whether the disposal constitutes a distribution. According to section 123(1) of the Companies Act, 2014 (as amended), a distribution is “every description of distribution of a company’s assets to members of the company, whether in cash or otherwise,” with certain exclusions like bonus shares or preference share redemptions. This is a description rather than a definition but in general, a distribution may arise where a company transfers an asset to a shareholder (or an entity controlled by a shareholder) for which it receives less than the market value of the asset. Nonetheless, deciding on the market value or relevant value for the asset can be uncertain, requiring consideration of Section 119 of the Companies Act, 2014.

The International Equal Pay Movement by Sandra Quinn

The reasons behind the gender pay gap are multifaceted, including factors like occupational segregation, lower representation of women in leadership roles, and maternity-related issues. The international equal pay movement seeks to address these disparities.

The international equal pay movement is not confined to a single country or region but encompasses global efforts to promote wage equality. Organisations such as the International Labour Organisation (ILO) and UN Women play significant roles in advancing this movement. Their initiatives focus on policy changes, data collection and analysis, and awareness campaigns to highlight the importance of equal pay.

Solicitors Accounts Regulations by Eamonn Maguire

A working group was established to identify amendments to the regulations which would copper-fasten the Law Society’s key responsibilities of protecting client moneys and the Law Society’s Compensation Fund. Such protections remain the primary purpose of all the accounting regulations mandated by the Solicitors Acts 1954 to 2015.

Finance & Management News

Finance & Management News

The scheme will be administered by Enterprise Ireland and is already open for applications. Co-funded by the Government and the European Regional Development Fund (ERDF), the funding will capitalize on existing regional enterprise partnerships and complement priorities set out in the nine Regional Enterprise Plans.

The scheme was launched at the beginning of this year and facilitates loans for working capital and medium-term investment to assist businesses with liquidity and in improving energy efficiency.

- This is a scheme for SMEs, primary producers, and small mid-caps (defined as businesses with up to 499 employees). SMEs are expected to be the main beneficiaries.

- To qualify for the scheme, the borrower will have to declare that costs have increased by a minimum of 10% on their 2020 figures and that the loan is being sought specifically as a result of difficulties being experienced due to the Ukraine crisis.

Finance & Management

Leadership Insight – Kelly Mackenzie

Kelly Mackenzie

In Dublin I worked with wonderful Irish clients like An Post and VHI. Having cut my teeth in the Irish design world I then took the leap to move abroad to Sydney, here I worked in Imagination and Landor, some of the largest agencies in the world. I developed my brand and experience… and really enjoyed the weather!

Deciding it was now time to get serious I moved to London. During my time there I really honed my branding skills and started playing a more strategic role in brand creation. I rebranded Cornetto Ice Cream, the first rebrand they had embarked on in over 50 years and worked closely with Lloyds of London, Unilever and The National Gallery before I left to set up my own agency. I had at this stage gotten to a point in my career where I felt I’d spent enough time working in other people’s agencies and building other people’s dreams that it was now time to go and build my own. So, I set up White Bear.

AIB partners with the Strategic Banking Corporation of Ireland by AIB

AIB now has loans under the Growth and Sustainability Loan Scheme, the latest SBCI loan scheme for both green and non-green lending for SMEs in Ireland. The Scheme is being introduced to encourage SMEs to invest in their businesses, drive productivity gains and to accelerate the transition to a more environmentally sustainable SME base.

June Butler, CEO of SBCI said “The SBCI welcomes AIB’s participation in the Growth and Sustainability Loan Scheme, as it means that Irish businesses, farmers and fishers have increased access to longer-term, lower-cost finance to fund their sustainable growth. Many businesses need the longer-term finance of up to 10 years made possible through the Growth and Sustainability Loan Scheme, to invest in strategic and ultimately sustainable growth. Loans provided by AIB will be at reduced interest rates and will be available unsecured up to €500,000.

FINANCIAL REPORTING

Financial Reporting News

Financial Reporting News

Financial Reporting updates and observations during 2023 by Phyllis Willoughby

The Financial Reporting Council (FRC) recently published its reporting expectations and monitoring findings for companies amidst a high period of interest rates, persistent inflation and ongoing economic uncertainty. Most frequently raised issues and areas of focus included:

- Impairments, judgments and estimates as this reflects the ongoing economic uncertainties companies need to factor into their financial reporting and the need for detailed explanations to help users understand the positions taken.

- Companies restating cash flow results.

- Review of Directors’ remuneration particularly regarding targets and performance against them

Irish SMEs need to address ‘investment gap’ by Mark O’Rourke

The good news is that growth feels achievable to Irish SMEs, with 72% saying they expect sales to increase in the next six months. They see attracting new customers (67%), building new supplier relationships (36%), taking on new staff (24%), renegotiating with existing suppliers (23%) and exploring new distribution channels (21%) as the key opportunities for the year ahead.

Taxation News

Taxation News

- Travel & Subsistence

- Small Benefit Exemption

- Remote Working Daily Allowance

To report these expenses/benefits, Employers and Agents will need Enhanced Reporting Requirements (ERR) permissions.

Employers will automatically be assigned ERR permissions via their existing ROS certificate. ERR permissions will not automatically apply to any sub certificates under the Employer certificate. The Employer must log into their ROS permissions screen to assign ERR accessibility to any sub certificate.

An additional Agent permission has been created to allow Agents to report ERR on behalf of their clients. Financial Agents will receive the ERR permissions automatically via their existing ROS certificate.

Non-Financial Agents will have to apply to Revenue for the ERR Agent certificate under their existing TAIN.

Budget Highlights 2024 by Mairéad Hennessy

The main announcements in Budget 2024 are:

There were no changes made to tax rates for 2024. The standard income tax rate will remain at 20% and the higher rate at 40%.

The Standard Rate Cut Off Points (SRCOP) for 2024 have been increased as follows:

In Practice News

Bye Law 7-Quality Assurance (QA)

Addressing of Quality Assurance recommendations

7.7-An emphasis is now placed on the requirement for firms and relevant individuals to take all reasonable steps to ensure that recommendations arising from quality assurance reviews are implemented within a reasonable period.

QA review selection process

7.12.1- The process for selecting firms and individuals for a QA review adopting a risk-based approach was expanded to incorporate those who were non-compliant with their obligations as a designated person under the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 as amended and where information was received from other regulators.

QA Shortened cycle

7.12.2-A QA review cycle of a firm may now be shortened where:

- two consecutive Grade Bs are scored by a firm in an audit review,

- where there is a failure to demonstrate adequate improvements within a reasonable time frame in any review area; or

- in any circumstance where there is a heightened risk associated in line with risk criterion.

Review Grades

7.17-Grade categories were expanded to introduce a “no grade” category. This is to be awarded where it is not possible to assess the adequacy and appropriateness of the quality of the engagement files undertaken by a firm or where a firm will not engage in the review process. This new category of grade also applies to Anti-money laundering, Continuous Professional Development and Investment Business reviews per Bye Laws 7.17.2, 7.17.3 and 7.17.4.

Thematic Reviews

7.23- The Bye Law was expanded to allow the completion of thematic reviews. Such reviews will undertake an assessment of a particular focus area and its implementation by firms and/or relevant individuals. These may occur on an ad-hoc basis and will be undertaken separate to the standard QA cycle review process.

IAASA Highlights Matters For Management by Maurice Barrett

The following business headlines from the rte.ie website for a single day in November 2023 illustrate the level of uncertainty:

PERSONAL DEVELOPMENT

The Professional Dilemma by Ben Rawal

As the audit neared completion, I met with the client to deliver my feedback prior to the report being issued. There were no significant control weaknesses. In fact, it was one of the strongest control environments that I had audited during my brief career, and I was pleased that I could give this feedback to the client. As per our standard reporting timescales, they would receive a draft report within ten working days. I remember leaving the client’s premises with a feeling of positivity having genuinely believed I had undertaken a good job.

Mind the Gap: Leveraging the Strengths of an Intergenerational Workplace by Dr Mary Collins

During my time as Head of Talent Development in Deloitte, I started to notice general differences in the drives and motivations of the graduates at the time (Gen Y) and realised we needed to flex and adapt our approach if we wanted to get the best from this powerful young generation. I went on to complete my doctoral studies in this topic and developed a framework to engage the youngest workplace generations. Over the last 10 years, I have been researching and writing about this topic and the challenges seem to amplify year on year as organisations face managing multiple generations under one roof with the added challenge of the hybrid workplace for most organisations.

The workplace has evolved into a melting pot of generations, each with its unique set of drives, motivations, and values. To harness the strengths of this intergenerational workplace, it is essential to first comprehend the distinct characteristics and expectations of each generation. In this article, we will delve into the four primary workplace generations: Baby Boomers, Generation X, Generation Y (commonly known as Millennials), and Generation Z (known as Centennials). We will explore their respective values, motivations, and how organisations can leverage their strengths to create a harmonious and productive work environment.

PERSONAL DEVELOPMENT

Specialisterne Ireland and the untapped talent pool by Specialisterne

Alarmingly, Ireland has the lowest rate of employment for people with disabilities in Europe at just 32.6%.

Getting back to the traditional interview and traditional hiring practices. Why don’t they work for neurodivergent people?

The emphasis on social interaction and communication skills presents a challenge. Many neurodivergent individuals struggle in this area, often underselling their achievements, having difficulty with eye contact or succumbing to interview anxiety. These same people might have a love of data, they might enjoy routine tasks that others find boring, they might love the nitty gritty detail that others shy away from. Sound like a great employee? Unfortunately, they can’t get past an interview.

Mindset Shaping and Goal Setting for Exam Success by Edel Walsh

This is a belief that many people live by, and it all comes down to your mindset. If you believe you can do something or achieve a goal, more often than not you will be successful. The opposite is also true. If you tell yourself, you can’t do something it can be a self-fulfilling prophecy.

Mindsets are powerful beliefs. There are two types of mindsets, the Fixed Mindset and the Growth Mindset. Carol Dweck, in her book “Mindset” says a fixed mindset is essentially a belief that your intelligence, talents and other abilities are set in stone. A person with a fixed mindset believes that they are born with a particular set of skills and that they can’t change them.

A growth mindset on the other hand is the belief that a person can develop their talents and achieve their goals through hard work, effective strategies, and support from others.

How to help your clients build the perfect tech stack by Frankie Jones, Pleo

As an accountant, you need to communicate to people who’ve been doing the same thing for 10 years that, in some cases, now it’s time to do things differently.

“The key is to make sure people understand why the change is happening and that the benefits, while they might be painful in the short term, will become apparent in the long run. It’s all about playing the long game,” recommends Graham.

Navigating Ethical Dimensions of AI and Upholding Integrity in Accountancy by Mark Butler

- Bias in Financial Decision-Making:

when not carefully designed, AI systems can inherit biases in their training data. These biases can result in unfair or discriminatory financial decisions. According to the HLB Cybersecurity Report 2023, 63% of surveyed businesses expressed concerns about AI bias and discrimination.

Harness the Future Through the CPA Metaverse, School of Innovation by Patricia O’Neill & Aisling Mooney

At the Skillnet Ireland Convention in April 2022 Susan Talbot of the Immersive Technology Skillnet and Camille Donegan, Director of Eirmersive cited that the retention rate for learning through immersive technology is 75%. This figure in itself is impressive but, when compared to the 5-10% retention rate for classroom learning, it is exceptional.

It is clear that the opportunities presented by immersive technology are extraordinary.

INSTITUTE

Institute News

Institute News

The samples are also a useful tool to support the ongoing training of staff and the production of high-quality financial statements.

CPD

CPD News

CPD News

Save the Dates for 2024

CPA Tax Conference 2024

Location: Online

CPD Credit: 8 hours

Cost: €225 (non-CPA members €275)

CPA Annual Conference 2024

Location: Hilton Kilmainham, Dublin & Online

CPD Credit: 8 hours

Cost: €225 (non-CPA members €275)

Irish Accountancy Conference 2024

Location: Online

CPD Credit: 8 hours

Cost: €225 (non-CPA members €275)

Student News

Student News

Newly Qualified Members

Training Records

On behalf of CPA Ireland, we would like to congratulate all of our students who were successful in their exams in August 2023.

Special congratulations to our prizewinning students who each achieved first place in their CPA examinations in 2023 (April and August sittings).

These resources include, for each paper:

- Detailed Syllabus and Learning Guide

- Past Papers and Suggested Solutions

- Relevant Articles

- Examinable Material

- Educators’ Briefing

Two new recently recorded webinars have been uploaded to this section of the website:

Information & Disclaimer & Publication Notices

Accountancy Plus is the official journal of the Institute of Certified Public Accountants in Ireland.

It acts as a primary means of communication between the Institute and its Members, Student Members and Affiliates and a copy is sent automatically as part of their annual subscription. Accountancy Plus is published on a quarterly basis.

The Institute of Certified Public Accountants in Ireland, CPA Ireland is one of the main Irish accountancy bodies, with in excess of 5,000 members and students. The CPA designation is the most commonly used designation worldwide for professional accountants and the Institute’s qualification enjoys wide international recognition.

The Institute’s membership operates in public practice, industry, financial services and the public sector and CPAs work in over 40 countries around the world.

The Institute is active in the profession at national and international level, participating in the Consultative Committee of Accountancy Bodies – Ireland – CCAB (I) and together with other leading accountancy bodies, the Institute was a founding member of the International Federation of Accountants (IFAC) – the worldwide body. The Institute is also a member of Accountancy Europe, the representative body for the main accountancy bodies The Institute’s Offices are at 17 Harcourt Street, Dublin 2, D02 W963 and at Unit 3, The Old Gasworks, Kilmorey Street, Newry, BT34 2DH.

The views expressed in items published in Accountancy Plus are those of the contributors and are not necessarily endorsed by the Institute, its Council or Editor. No responsibility for loss occasioned to any person acting or refraining to act as a result of material contained in this publication can be accepted by the Institute of Certified Public Accountants in Ireland.

The information contained in this magazine is to be used as a guide. For further information you should speak to your CPA professional advisor. Neither the Institute of Certified Public Accountants in Ireland or contributors can be held liable for any error, or for the consequences of any action, or lack of action arising from this magazine.

The Investigation Committee found prima facie evidence of misconduct by Mr. Edward Kelly; and Eddie Kelly & Co of No. 2 Dair Ard; Bohreen Hill, Enniscorthy, Co. Wexford in relation to the following complaints:

1. Quality Assurance Complaint

Failure to carry out work in accordance with approved auditing, accounting and quality management standards – Bye law 7.4 , bye law 6.6.1 (a) and Section113 – Professional Competence and Due Care of Code of Ethics refer.

Failure to implement recommendations following quality assurance review conducted in 2019 – Section 1496 of Companies Act 2014 refers.

2. Breach of Hot File Review condition

Breach of a hot file review condition imposed in accordance with bye law 7.17.3 – Bye Law 7.17.3, bye law 6.5.1 (a) and Section 115 – Professional Behaviour of the Code of Ethics refer.

3. CPD

Failure to take part in appropriate programmes of continuing education in order to maintain theoretical knowledge, professional skills and values, particularly in relation to auditing at a sufficiently high level – Bye Law 13.33.3 and Section 1489 of Companies Act 2014 refer.

The Committee offered and the Member accepted, a Consent Order, the terms of which are as follows:

- Reprimand;

- Fine €2,000

- Contribution of €3,000 towards the Institute’s costs in this case and

- That details of the Consent Order be published in Accountancy Plus with reference to the Member and Firm by name.

Dated: 21st September 2023